News

Capelin Fishing in Iceland: A Strong Recovery After Two Challenging Years

After two consecutive years of severe disruption, Iceland’s capelin fishery is heading into a markedly stronger season in 2025/2026. New results from extensive winter surveys conducted in January 2026 indicate a significantly larger capelin stock than initially expected, paving the way for a revitalized fishing season with substantial economic and social impact.

Survey Results and Stock Assessment

Survey Results and Stock Assessment

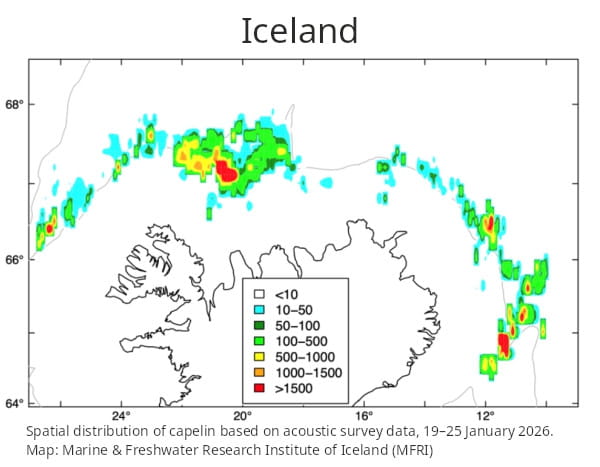

The Marine & Freshwater Research Institute (MFRI) completed its winter capelin surveys between 19 and 25 January 2026. The surveys covered a wide area to the northwest, north, northeast, and east of Iceland and were carried out with the participation of five research vessels. Conditions during the survey period were favourable, with neither weather nor sea ice significantly affecting the measurements.

The total spawning stock biomass was estimated at approximately 710,000 tonnes, indicating a clear improvement compared to recent years. Capelin were found to be widely distributed across the survey area, with the highest densities observed in the leading edge of the spawning migration east of Iceland and offshore from Húnaflói.

Based on the current harvest control rules agreed upon by the coastal states, and drawing on both the autumn 2025 survey and the January 2026 winter survey, MFRI has recommended that total catches for the 2025/2026 fishing year should not exceed 197,474 tonnes. This represents a more than fourfold increase from the initial quota of just under 50,000 tonnes announced earlier in the season.

A Sharp Contrast to Recent Years

The new quota marks a dramatic turnaround from the previous two capelin seasons, both of which were characterized by near-total failure. In those years, stock levels were insufficient to support a viable fishery, resulting in lost income, idle vessels, reduced processing activity, and significant uncertainty in many coastal communities.

Even at the start of the current season, expectations were modest. The initial quota of approximately 44,000 tonnes reflected continued caution and uncertainty regarding the stock. However, follow-up surveys after the New Year revealed a much stronger spawning stock than previously detected, fundamentally changing the outlook for the season.

This recovery does not yet signal a return to historically large capelin years, but it does represent a meaningful break from the prolonged scarcity that has affected the industry in recent times.

Quota Allocation Among Coastal States

Quota Allocation Among Coastal States

Under existing international arrangements, the capelin quota is shared among Iceland, Greenland, Norway, and the Faroe Islands. Iceland receives by far the largest share, just over three quarters of the total quota, equivalent to roughly 150,000 tonnes. This allocation reflects Iceland’s central role in the fishery and the proximity of the main spawning migration to Icelandic waters.

The remaining quota is divided among the other coastal states, each of which participates in the management of this migratory stock.

Economic Impact and Export Markets

The improved capelin season is expected to have a substantial positive impact on Iceland’s economy. Export revenues from the fishery are estimated to reach 35–40 billion ISK, a sharp increase compared to recent years when capelin exports were minimal or non-existent.

Markets have become increasingly undersupplied after several weak seasons, creating strong demand and favourable pricing conditions. The focus this season is expected to be firmly on human consumption markets, which offer significantly higher value than industrial uses such as fishmeal and oil.

Asian markets, particularly in East Asia, are of central importance for roe-bearing capelin. Capelin roe, commonly known as masago, is widely used in sushi and other seafood products and commands premium prices. At the same time, Eastern European markets remain important for male capelin, providing additional market diversity and stability.

Because the overall quota remains limited despite the increase, fishing strategies are expected to prioritize quality and timing. Vessels are likely to wait until roe development reaches optimal levels before commencing large-scale fishing, ensuring that the catch can be directed toward the most valuable product categories.

Timing of the Spawning Migration

Approximately 54% of the measured stock, around 382,000 tonnes, was detected east of Iceland and is expected to follow the traditional spawning migration southward and westward along the coast. The remaining 46%, or 328,000 tonnes, was measured northwest of the country.

At present, some uncertainty remains regarding the migration route of the northwestern component of the stock. It is not yet clear whether this portion will spawn north of Iceland, west of the country, or join the eastern migration route later in the season. Further research surveys planned for February aim to clarify this movement.

Due to this uncertainty, authorities have advised that fishing should take place both off the north coast and in eastern waters, rather than focusing solely on the stock component already progressing along the eastern route.

If the migration develops as expected, capelin are likely to move along Iceland’s south coast within the coming weeks, with peak fishing opportunities emerging later in the season as roe development improves.

Social and Regional Significance

Beyond export revenues, the capelin season plays a critical role in sustaining employment and economic activity in coastal communities. Fishing vessels, processing plants, ports, and municipalities all benefit directly from a successful season.

For many communities, capelin fishing provides intensive employment for a concentrated period of six to eight weeks, supporting hundreds of jobs both at sea and on land. After two years of disappointment, the improved outlook has brought renewed optimism and financial relief to regions that are highly dependent on seasonal fisheries.

A Cautious but Optimistic Outlook

While the current season represents a welcome recovery, fisheries management remains firmly grounded in precaution. The recommended quota reflects both the improved stock estimate and the need to ensure long-term sustainability in a fishery known for its natural variability.

The 2025/2026 capelin season is therefore best understood as a rebuilding phase rather than a full return to abundance. Nevertheless, after years of scarcity, the combination of a viable quota, strong markets, and favourable survey results marks an important step forward for Iceland’s capelin industry.

The tags below provide an opportunity to view previously posted related news within the selected category